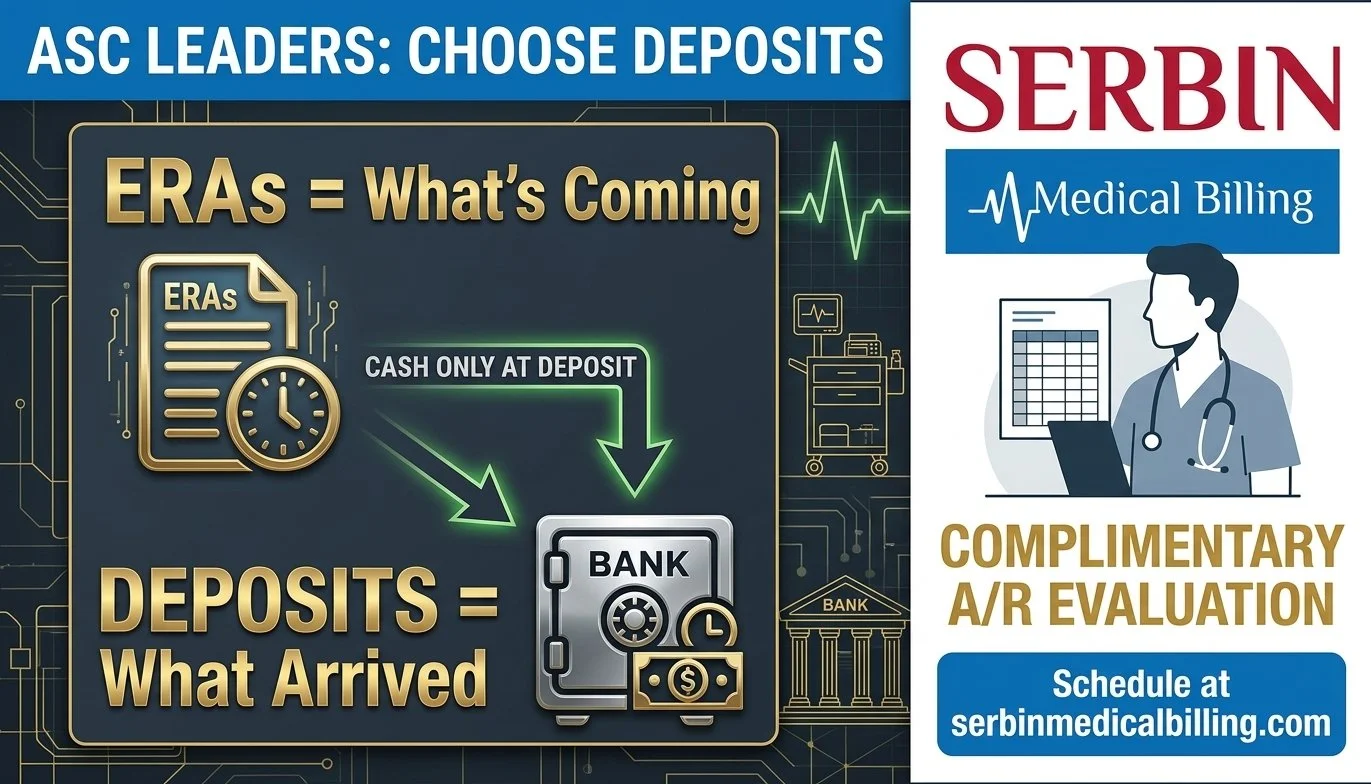

ERAs Tell You What's Coming. The Bank Tells You What Arrived.

In ambulatory surgery centers (ASCs), accurate payment posting is the foundation of trustworthy financial reporting. Yet a common and costly mistake still occurs across revenue cycle operations: posting payments based on the date the payment is processed or posted, rather than ensuring that payments reconcile exactly to the bank statement.

Posting to the bank statement is not just an accounting preference. It is a financial control requirement that affects cash accuracy, audit readiness, payer follow-up, and executive decision-making. ERAs tell an ASC what is coming. The bank tells it what actually arrived.

The Core Principle: Cash Is Real Only When It Hits the Bank

From an accounting and compliance perspective, cash is not received when an EOB is generated, when a payment is posted in the billing system, or when a file is transmitted via ERA. Cash is received only when funds are deposited and cleared by the bank. For this reason, payment posting must reconcile to the bank statement, ensuring that every dollar reflected in the billing system matches actual cash received.

The Risk of Posting by Processing Date

Many ASCs post payments using ERA receipt dates, check receipt dates, or posting batch dates. While operationally convenient, this approach creates several risks.

Cash Overstatement or Understatement

Payments often appear on ERAs days before funds settle, batch across month-end, or are reversed or adjusted before clearing. Posting ahead of bank settlement can inflate cash balances or distort monthly financials.

Month-End and Year-End Misstatements

When payments are posted before they appear on the bank statement, revenue may appear in the wrong accounting period, month-end close becomes unreliable, and financial statements fail audit scrutiny. This becomes especially problematic during year-end reporting, distributions, or financing events.

Reconciliation Breakdowns

If posting does not tie directly to deposits, bank reconciliations become manual and time-consuming, differences are harder to trace, and small errors compound into material discrepancies. Over time, finance teams lose confidence in reported cash.

Why Bank-Based Posting Is a Critical Internal Control

Posting to the bank statement creates a closed control loop. Payment is deposited, the deposit appears on the bank statement, the deposit total is posted in the billing system, and the posting ties exactly to bank activity.

This control prevents phantom or duplicate postings, detects missing or misapplied payments, supports segregation of duties between posting and reconciliation, and replaces assumption with verification. For ASCs with multiple payers, locations, or lockbox arrangements, this control is non-negotiable.

Operational Benefits for Revenue Cycle Teams

When posting aligns with bank deposits, unpaid claims stand out clearly, missing ERA payments are identified faster, and secondary billing timing improves. Bank-based posting also quickly surfaces reversed ACH transactions, recoupments or offsets, and short pays embedded in bulk deposits. Teams spend less time chasing pennies and more time resolving true cash gaps.

Audit and Compliance Implications

Auditors expect healthcare entities, including ASCs, to reconcile cash receipts to bank statements, demonstrate clear payment audit trails, and prevent timing differences that misstate cash. Posting by processing date undermines this expectation and raises red flags during external financial audits, payer audits, ownership transitions, and sale or merger diligence. Bank-balanced posting demonstrates financial discipline and control maturity.

Best Practices for ASC Payment Posting

Post by Deposit, Not by ERA Date

Use the bank deposit date as the authoritative record for payment posting, regardless of when the ERA was received or processed.

Tie Every Batch to a Bank Total

Every posting batch should match a specific deposit, balance to the penny, and remain traceable back to the bank statement.

Separate Posting and Reconciliation Duties

Financial integrity is strongest when one team posts payments and another team reconciles to the bank.

Document Timing Differences

When deposits cross accounting periods, document deposit dates, posting delays, and the reason for variance. Transparency protects against future disputes or audits.

Final Takeaway

In ASC finance, payment posting accuracy is not about speed. It is about trust. Posting payments based on when they are processed may feel operationally efficient, but it introduces financial risk, audit exposure, and reporting uncertainty. Posting that balances directly to the bank statement ensures accurate cash reporting, clean reconciliations, strong internal controls, and confident executive decisions. When it comes to ASC payment posting, the bank, not the processing date, is the source of truth.

Frequently Asked Questions

Why should ASCs post payments based on the bank statement instead of the ERA date?

Because cash is only real when funds clear the bank. Posting by ERA or processing date can inflate cash balances, distort month-end financials, and create timing differences that fail audit scrutiny.

What internal control benefits does bank-based posting provide?

It creates a closed control loop that prevents phantom or duplicate postings, detects missing or misapplied payments, and supports clear segregation of duties between posting and reconciliation.

How should ASCs handle deposits that cross accounting periods?

Document the deposit date, the posting delay, and the reason for the variance. Transparency about timing differences protects against future audit findings, ownership transitions, and payer disputes.

Strengthen Your Payment Posting Process

Serbin Medical Billing helps ASCs navigate payment posting workflows, analyze reconciliation gaps, and identify the controls that protect cash accuracy. To schedule your complimentary A/R and revenue cycle evaluation, contact us today!